After a year of detours, Abengoa's actions seem to be in a lethargy. Last summer the price was at a standstill. In which an attempt was made to remove the minosristas from the price and then buy back in the lower part.

After the summer Abengoa would start looking for a partner with whom to share the weight of the debt and who can try to help in the search for new projects. What was offered by the company was not attractive enough since no group showed the least interest. For which Abengoa would contract the investment bank Lazard .

Since then, Abengoa has been very opaque in showing any information and, at a quote, it has been oscillating around the cent. This is possibly due to the fact that he still has quite a few pending things, such as awards to win and fines to pay. The most damaging fine could come from the European Union for altering ethanol prices .

It is also pending several awards. The most important against the Spanish State because of the cut in subsidies for renewables . This lawsuit is over 5 years old although all the lawsuits are being resolved this year and almost all of them have been favorable to the plaintiffs. Abengoa sold the litigation to a fund last year, securing some 75 million even though the trial was unfavorable and an amount of 25% on its benefit, seeing that it could take more than a year. However, by continuing the previous government and seeing that it is very prone to increase items to renewable energy, it has returned to take control. The government could have reached an agreement for the claimed money to go down but to be favorable to the company's interests. The money requested that can reach 1,500 million euros could totally change the company's price, which barely exceeded 350 million euros. Being able to multiply in case of winning half about 600 million in 2 or 3 times the price.

As for the debt, the most important thing is that it has closed an agreement with its creditors in both Mexico and Brazil and all the debt associated with it could disappear this year, and could be around 2.5 billion euros .

Below I show the debt of the company that has barely changed after the restructuring of last year, waiting for them to present the current total in the annual results of 2019 that have been delayed for more than a month.

| ### | 2019 | 2018 | Observations | |

|---|---|---|---|---|

| Corporate Financial Debt | New Money 1 | 368 | 668 | Part of 1266 M of Feb 2017 (5% 2 years) | New Money 2 | 262 | 267 | Part of 1266 M of Feb 2017 (5% 2 years) | Old Money | 2714 | 1556 | Money back to agreement before 2017, limit 2022-2023 and low interest rate |

| Loan Las Palmas | 77 | 77 | Short term, reserved | |

| Mexican debt | 217 | 213 | Short term | |

| Overdue confirming | 15 | 16 | Recent debt to pay soon | |

| Guarantees | 85 | 78 | Short term | |

| Derivatives | 21 | 22 | Short term | |

| Other corporate debt | 649 | 569 | 75% Short term - 25% long term | |

| Total deuda financiera | 4407 | 3558 | ||

| Proyect Finance | 320 | 111 | Long term | |

| Debt companies held for sale | 929 | 1129 | Short term | |

| Total Financial Debt | 5656 | 4698 | ||

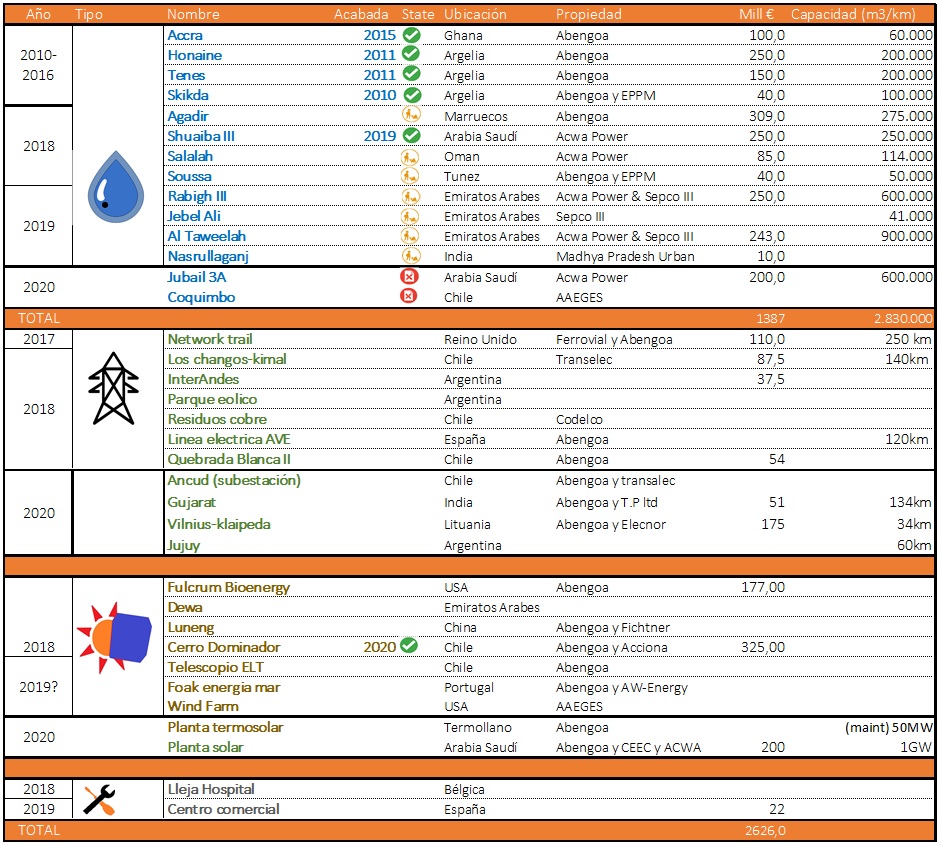

In the part of contracts we would go with some new contracts, although last year a great workload was gained, which also cannot absorb so many contracts this year.

The new desalination plant stands out, and the contracts in South America in which, after the completion of Cerro Dominador this year, it is becoming a benchmark in the entire field around the sustainable world

It has recently won new jobs in terms of power lines in Brazil, which leads it to return to operating in the country after the sale of all the lines it had unfinished due to the bankruptcy of the subsidiary in that country.

Thus, Abengoa has improved this year with respect to the previous one, mainly due to the end of the creditor processes and for having much more favorable awards (having won two of them last year for a value close to 100 millions of euros). Due to all these components, Abengoa's price is very adrift, with a large margin for improvement but also the risk of running out of liquidity again.

In fact, currently, after the COVID crisis, it is negotiating with creditors and bondholders to win a small loan of around 50 million to be able to negotiate new future projects. And it is that Abengoa, like the rest of the companies, has had to carry out an ERTE to avoid losses of around 100 million euros, which are essential for the viability of the company.

The technical analysis in the quotation makes no sense since it hardly makes consistent movements. The volume traded in euros has decreased a lot since the first half of 2019. It moves with very little volume since no major investor has the slightest interest in it. Right now, like all companies, it is trying to recover the price it had before COVID19, which was around the cent.

Since no one on the board of directors has a direct stake in the company and the company is currently owned by creditors (several banks), the listing of the company reflects only little interest in the value. What matters most is whether the creditors are going to collect their share. These have already made an investment last year to finish A3T and would be about to close this divestment this year. Although after COVID everything has been left in the air since any investment by a large is going to be looked at with a magnifying glass.

Due to the wide range of companies with problems and which are quite undervalued, Abengoa will now have less prominence and there could be other companies that can significantly reduce their assets. That together companies that are below their book value quoted on the stock exchange makes postpone the horizon of comeback of the company in the listing. There is no point in doing a technical analysis.

© 2016 - All Rights Reserved - Diseñada por Sergio López Martínez

![[Valid RSS]](https://www.onepointsync.com/wp-content/uploads/2016/08/valid-rss-rogers.png "Validate my RSS feed")