Abengoa no vive su mejor momento. Tras el secuestro de la acción por la CNMV a las ordenes de la élite empresarial del país ha estado cerca de desaparecer. A día de hoy ha surgido una plataforma que reúne a los principales accionistas del grupo, con cerca del 25%. Este grupo pretende reorganizar la empresa, con el fin de salvarla de su desaparición y poder salvar miles de puestos de trabajo. Se tendría que negociar con los principales acreedores y bonistas que cargan con una gran deuda que esta lastrando los resultados de la compañía. Estos acreedores no quisieron la liquidación de la empresa y se desvincularon de ella mediante la venta de sus acciones. Hicieron caja y además han venido percibiendo numerosos pluses de los beneficios durante estos 3 años. Por si fuera poco, son los responsables de la situación que viven los trabajadores de la empresa, que son victimas colaterales de la situación, con recortes de sueldo y suspensión de pagas.

In 2018, after carrying out the refinancing, loose ends would be left for the possible sale of Abengoa before 2023. What nobody knew is that after the covid, and in the absence of actions by the Spanish regulator, Abengoa would stop responding to investors, and would not present accounts anymore. The council that was at the time at the head of Gonzalez Urquijo could be presented to years of disqualification if instead of the Spanish market it were the American one.

Documentary falsification and the manipulation of the value of the share could weigh among several crimes. The falsehood could not yet occur since as of today, 2021, the audited accounts for 2019 have not been presented, let alone those for 2020.

Opportunism arose before the covid and an attempt was made to end the problem that the company was dragging on, which is its high exposure to high interest rates for the old debt. The plan consisted of yielding very bad results and arguing very bad forecasts due to the coronavirus crisis to access European loans. This loan would consist of about 500 million euros, given from the Spanish state through the ICO (Official Credit Institute), 250 million and from the SEPI (State Society of Industrial Participations) about 20 million (requested in principle to the board and due to the refusal to this entity).

Y es que el novel gobierno de Andalucía, liderado por Juan Manuel Moreno Bonilla, habría evitado este apoyo sabiendo en las consecuencias legales que puede acarrear. El partido al que sustituye, el PSOE, ha realizado multitud de concesiones en el pasado a la empresa andaluza y todavía no se sabe que ha pasado estos años. La situación de la empresa es muy parecida a la que ha estado inmersa Andalucía tras años de un robo sistémico por parte de la administración y altos cargos de la junta han respondido a la justicia. En Abengoa todavía estaría por ver que papel han jugado, ya que actualmente los consejeros de la empresa habrían estado colocados por la banca acreedora y por el Gobierno español de turno.

Y es que el novel gobierno de Andalucía, liderado por Juan Manuel Moreno Bonilla, habría evitado este apoyo sabiendo en las consecuencias legales que puede acarrear. El partido al que sustituye, el PSOE, ha realizado multitud de concesiones en el pasado a la empresa andaluza y todavía no se sabe que ha pasado estos años. La situación de la empresa es muy parecida a la que ha estado inmersa Andalucía tras años de un robo sistémico por parte de la administración y altos cargos de la junta han respondido a la justicia. En Abengoa todavía estaría por ver que papel han jugado, ya que actualmente los consejeros de la empresa habrían estado colocados por la banca acreedora y por el Gobierno español de turno.

"Entre varios delitos podrían pesar la falsedad documental, y la manipulación del valor de la acción".

The current situation of technical bankruptcy would be caused by the high debt of the company. Nothing new under the sun, that debt was already considered last year and in the report they made at the end of 2019, the only thing that intentionally devalued the assets to place Abengoa as a non-viable long-term company . In addition to seeking the granting of these gifted loans, it would be sought that the creditors would control the company by issuing new shares, leaving the former owners out of the operation.

The debt presented before the coronavirus and after is the same although, the liability, even higher before because they had reduced debt. The point is that the valuation of assets (net worth) at 4,400 million in March 2019 was no longer such, and they cut that value as much as possible, making the group's total liabilities rise a lot as you can see in the following image. 2019 liabilities presented in progress and in 2020 in red square.

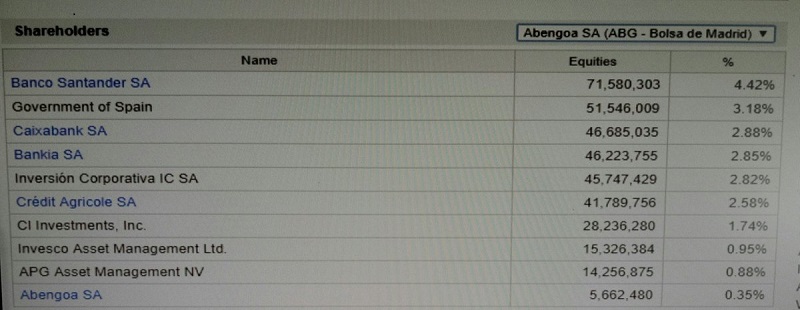

La perdida de los accionistas en Abengoa no tiene parangon en el mercado español, habiendo caído la acción desde 1 euro actual a un cerca de un céntimo y tras el covid ha llegado a estar cerca de la centésima parte del céntimo, rondando los 60M de euros. El consejo de abengoa afirma que esta valoración se debe al peso de la deuda, pero justamente empezo a afirmar esto después de la operación Acordeón en 2017 en la que la banca se deshizo de titulos de abengoa a 4 veces mayor que el precio que debían tener para amortizar sus pérdidas habiendo realizado una operación en los medios para incitar a la compra. Entre estos bancos estan Caixabank, Bankia, Santander, o Credit Agricole.

La perdida de los accionistas en Abengoa no tiene parangon en el mercado español, habiendo caído la acción desde 1 euro actual a un cerca de un céntimo y tras el covid ha llegado a estar cerca de la centésima parte del céntimo, rondando los 60M de euros. El consejo de abengoa afirma que esta valoración se debe al peso de la deuda, pero justamente empezo a afirmar esto después de la operación Acordeón en 2017 en la que la banca se deshizo de titulos de abengoa a 4 veces mayor que el precio que debían tener para amortizar sus pérdidas habiendo realizado una operación en los medios para incitar a la compra. Entre estos bancos estan Caixabank, Bankia, Santander, o Credit Agricole.

Few cases have precedent for this. And the CNMV has done practically nothing. A manipulation of a value that just last year presented an EBDITA of 300 million euros. A price that would be equivalent to about 3,000 million. Without going any further, Solaria in the continuum capitalizes today, January 6, 2021, about 3,500 million and has a much lower EBITDA of close to 30 million euros.

"A manipulation of a value that just last year presented an EBDIT of 300 million euros ..

These actions are classified as seizure of assets and those responsible could face prison terms. Even so, having practically bought justice, this and more cases have already been taken into account for a long time. The operation that they wanted to carry out in 2023 took into account numerous expenses and the concession of a part of the benefits to those shareholders who complained before the judge. In the end, this way is much cheaper for banks than paying shareholders, as has been the case with Banco Popular.

These actions are classified as seizure of assets and those responsible could face prison terms. Even so, having practically bought justice, this and more cases have already been taken into account for a long time. The operation that they wanted to carry out in 2023 took into account numerous expenses and the concession of a part of the benefits to those shareholders who complained before the judge. In the end, this way is much cheaper for banks than paying shareholders, as has been the case with Banco Popular.

"These actions are classified as seizure of assets and those responsible could face prison terms.".

To stop these misconduct, a shareholders association called Abengoashares has emerged that fights for the interests of Abengoa shareholders.

© 2016 - All Rights Reserved - Diseñada por Sergio López Martínez

![[Valid RSS]](https://www.onepointsync.com/wp-content/uploads/2016/08/valid-rss-rogers.png "Validate my RSS feed")