Abengoa is a leading Spanish company in the renewable energy sector and has diversified its activities in different sectors such as energy maintenance and drinking water supply through the construction of desalination plants. This diversification has been carried out to save the company due to the technical bankruptcy it was in.

In 1996 it would begin to quote in the continuum and in 2008 it would give its jump in the IBEX35 where it would leave in 2015 after falling its quotation more than 200% in few months happening of the 4 € to near the euro.

Since then many things have happened that have been told from this page. First of all the agreement of creditors that would be signed in 2017, thanks to the agreement of the old leadership with bankers and the state . Then the value would suffer a remarkable correction. Not only because of the effect of dilution but also because of the sale to the market of most of the capital donated to banks. This strategy left the value in a coma, touching the cent and thousands of Spanish minority investors in the ruin. Although it has to be said that whenever someone sells someone buys. And that's where agencies with information very close to Santander were playing their cards to get the maximum benefit from those operations, many of which were short positions.

After several extraordinary meetings, agreements would be reached to sell the company's most important assets, such as Atlantica Yield, and to finish the sale of A3T. The latter would need endorsements from Banco Santander in order to be finalized and sold at the best price. That yes, charging its corresponding part.

The biggest headache for the company led by Gonzalo Urquijo , one of the best Spanish business managers that was put unanimously after the 2017 agreement, has been the impugning ones that did not sign precisely that agreement. These did not suppose more than 3% and the company I throw a pulse to the same that I end up losing after the judgment of the judge in his favor, in summer of 2017. Since then the company has been trying to convince him with numerous offers and it has not been precisely until now that after many efforts of the members of Abengoa that has been carried out . Likewise, the price of the company has continued to suffer the consequences, reaching an unprecedented fact. The fall in value below the admissible value of the Spanish markets. With the approval of the CNMV, BME modified the statutes of the Spanish stock exchange to reduce the size by blocks of the value orders and mark the minimum at 10 times the value, the hundredth of a cent of a euro being the minimum value.

To this measure, all minority associations and Abengoa itself were directly opposed, since due to the moment when they were in need of time to reach an agreement with all the parties. BME would apply the change in October of last year and the share would fall to € 0.0021 . This would be a psychological stick for anyone who had actions within, both to sell and to buy since no one knew for sure what was the limit where the action could fall. The company at that time was worth almost 60 million euros .

Since then the negotiations have been successful and the restructuring of the debt has been carried out successfully. By 2018 the debt was structured:

| ### | 2019 | 2018 | Observations | |

|---|---|---|---|---|

| Corporate Financial Debt | New Money 1 | 368 | 668 | Part of 1266 M of Feb 2017 (5% 2 years) | New Money 2 | 262 | 267 | Part of 1266 M of Feb 2017 (5% 2 years) | Old Money | 2714 | 1556 | Money back to agreement before 2017, limit 2022-2023 and low interest rate |

| Loan Las Palmas | 77 | 77 | Short term, reserved | |

| Mexican debt | 217 | 213 | Short term | |

| Overdue confirming | 15 | 16 | Recent debt to pay soon | |

| Guarantees | 85 | 78 | Short term | |

| Derivatives | 21 | 22 | Short term | |

| Other corporate debt | 649 | 569 | 75% Short term - 25% long term | |

| Total deuda financiera | 4407 | 3558 | ||

| Proyect Finance | 320 | 111 | Long term | |

| Debt companies held for sale | 929 | 1129 | Short term | |

| Total Financial Debt | 5656 | 4698 | ||

As we can see, this is the new financial debt, with 4407 million gross. Which will be reduced soon in 200 million after the sale of A3T that is now supported by Santander bank after an injection of 143 million less than 6 months ago.

The new thing is that the terms are increased and the previously demanded interests that should have already begun to have very high interests of 10% are lowered. If this had been done, the viability of the company would not have been possible. To this end, the company structure has been divided, passing 73% to a second company called AbNewCo 1. Banco Santander now holds 8% of the company and the rest is part of the creditors virtually. If the company meets the objectives set, the company will not become part of the creditors and bondholders. These 143 million will be returned soon after the sale of A3T.

The expected EBDITA is 6.5% 7% annually for the next few years. The results of this first four-month period have been in line with what was expected. With a loss of 150 million due to all this time lost with the restructuring and the search for project financing. After the completion of these milestones, three major contracts have been achieved, which will be detailed later when the project portfolio is shown. To address this debt, the following route has been set:

If we look, we can see that EBDITA expected for this year is 164 million euros to fulfill the plan . This result is quite pessimistic since according to my accounts it will be close to 200 million this year. In fact, an EBDITA of 47 million has already been reached until April. Comparing the results with the same periods of the previous year we can see a slight improvement accounting for an increase in cash and a change in trend in which the number of people hired that is increasing and is very close to 12,000 people We must remember that we have been two consecutive years of increases in the EBDITA from 127 million in 2017 to 188 in 2018. Calculations in 2020 should generate an EBITDA close to 300 million although the 10-year plan is very conservative to avoid possible risks. It puts it at 194 million so if the 300 million that I calculate were reached, the price of the stock should rise vertiginously and reach by 2020 a value close to 1,000 million. Abengoa's price is currently at 300 million with what would be a revaluation close to 400% .

Normally, the price of an action is calculated in relation to the EBDITA, multiplying the value of the company by 10. However, in our case, due to the large debt of the company, the debt / EBITDA indicator should be taken into account, which is quite negative but that has been improving slightly these years.

The 'EBITDA' is the best approach to the cash generated by a business, and the cash is a concept that everyone understands well. It is calculated in an Income Statement, subtracting all the expenses that require disbursement to the income, and not therefore the amortizations, since they do not involve cash outflow, and without taking into account the financial debt, that is, without subtracting the expenses financial .

If we take into account this indicator and next year exceeds 300 million and debt is repaid in the remaining divestments we would be talking about having a company with a short-term debt of less than 1,000 million. Currently this debt is around 1,500 million euros. This reduction of debt would have an impact on the value of the company and even before this happens, this fact will be already discounted.

In order to calculate this data, it would be necessary to observe the business portfolio and make a range of benefits in order to know where Abengoa can walk next. As if it was not enough after the restructuring Santander bank would be willing to contribute punctually in the financing of new projects that may arise . This could bring for this year still some great contract more that marks the difference with respect to the near future that is quite good to another one in which the debt happens to form history.

They would also be on the ship right now new banking entities such as BBVA and Bankinter having participated in the guarantee of 140 million . If the banks decide to support Abengoa with quite negative accounts, let's imagine when they start to raise ECB rates and the profits of these begin to rise considerably. So it will be much easier to support new projects although the cost will surely increase.

Another important point is the entry into this support of Carlos Slim, owner of the company FCC and greater fortune of Mejico . It would have begun to provide financial support but it would not rule out entry into the shareholding. This could bring internal fights over Abengoa's control and perhaps in the future bring a possible prior takeover bid for a capital increase of the company.

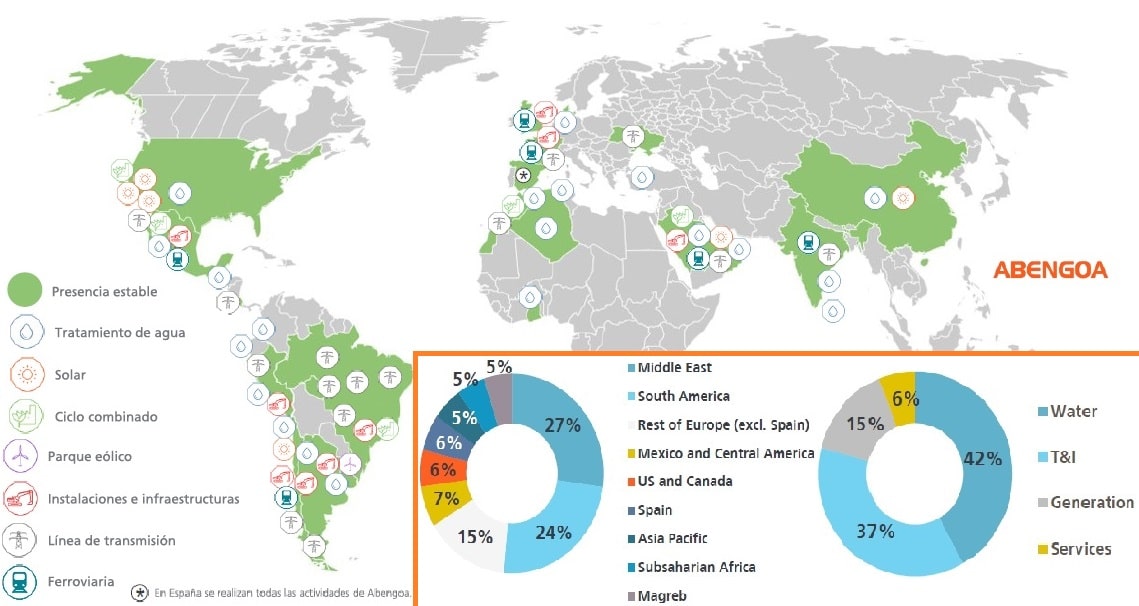

Abengoa has a presence throughout the world, having moved from a business portfolio based on renewable energies and the installation of power plants to one based on water treatment, desalination and electric transmission lines. The current portfolio is diversified in countries as follows:

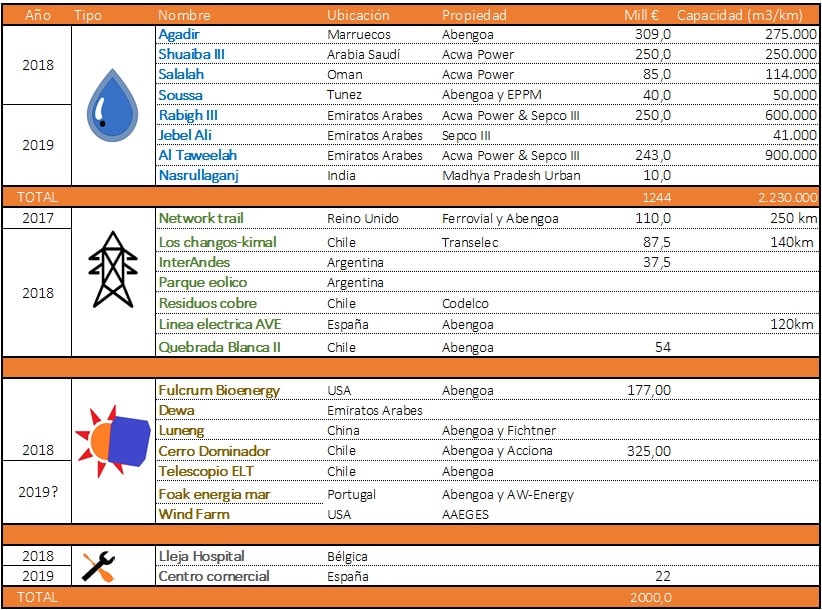

South America and the Middle East being the main focus of projects of the new Abengoa in which practically 50% of the workforce is currently working. Below I show Abengoa's current project portfolio with several projects that exceed the capitalization of the same. The current amount is close to 2,000 million euros in large projects to which should be added those smaller than the Abengoa contracts such as Abeinsa for example.

As relevant projects you would find the one signed for Indian water treatment which is the first foot in a country with a lot of project needs and with the highest annual GDP growth in the world . It has been carried out thanks in part to the trip made by the foreign minister, Javier Borrell last year. This would be to plant the pike in one of the most interesting and future fields, water but in one of the countries with the most needs. is that the same Michael Burry who came forward to The great financial crisis of 2008 due largely to subprime mortgages has been invested since then and researching the water sector that has much more power than renewable energy or the electric car.

According to the United Nations, the use of water has grown twice as fast as the growth of the world population during the last century. As of today, we are using 30% of the available drinking water in the world. In less than 10 years the use will increase to 70%. In 2025, 1,800 million people will live in areas where potable water will be scarce and 2/3 of the world's population will be in areas where they will have short-term stress of lack of water.

Other interesting projects would be the largest telescope in the world in Chile that would be pending bidding , when it confirms the completion of the building where it will be located and a new project in the USA in collaboration with AEGES for a large wind farm that could come out in the coming months . A year of elections in the US it is foreseeable that in the coming weeks the great plan of infrastructures promised in the electoral campaign for the amount of 1 billion dollars will be launched. Maybe that's where Abengoa can get something through Algonquin since Atlantica is an American company and therefore unimpeded to enter projects due to Trump's well-known protectionist policies.

Taking a big step right now in the Middle East and South America would be to increase exposure to the Asian market, China and India and sign more projects with the new alliance (AEGES) with the Canadian company that bought Atlantica Yield.

If in these projects a net profit will be obtained, being optimistic of 20% we would give an EBDITA in these two years of about 400 million to which we would have to add projects that are incorporated later. The point is that these first two years are vital and if the projects are executed correctly, a new investor could knock on the door with the intention of taking a great weight in the company and willing to reduce the debt of the same, multiplying the price of the company if it were for 4. Abengoa is fundamentally one of the most attractive companies in the Spanish market, quoting at prices well below the size of the company and the volume of business. The big question is the evolution of the company in the short term and if it realizes the assigned projects in a correct way and in the foreseen terms. For this, it has a fairly good management and advice led by Gonzalo Urquijo, one of the most prestigious businessmen in Spain who has refloated several companies before, especially ArcelorMittal.

So Abengoa has all the wind in its favor. In addition, the ECB has not yet moved a finger for the rate hike so the debt to date has quite low interest rates.

Abengoa has spent these two years since the agreement of creditors for a stock market inferno. Harassed by the shorts and by the massive sale of the shares given to the banks, the stock came to be worth the minimum valid for BME, the private operator that manages the Spanish stock market.

It would oscillate very little by news of contracts won that would be the perfect scenario for the sale of the great ones to minorities. After 6 months with hardly any movements in the B shares of the company and Abengoa A having dropped below 2 cents, the regulation would be modified. Reducing Abengoa to the minimum expression, 60 million capitalization .

A few unsuspecting would sell after this measure to € 0.0035, for four or five times less the value they paid for it. Mostly I would sell people who bought the cent, the last to enter Abengoa and who preferred to lose half to risk losing everything. On the other hand, the agencies that carry out the operations in Abengoa would receive the shares as gold in cloth and after the new year and the negotiations with the creditors, the share price would take off until the psychological value of the cent per share was recovered. Many of us who came from above we averaged before the cent. In my case at 0.0068 and 0.0081, having my first big purchase at 2.2 cents and my second big purchase at 0.013 cents having achieved an average that is close to recent highs of 0.0147.

If we count the number of shareholders that we are buying in Abengoa, the figure is not very high and it is a loss that can be assumed by those who see value in the company. The strategy now is to monitor the means and the MACD indicator to close positions when necessary and thus reduce the%. According to my calculations this year the retailers that have executed the operations well should come out positive.

If we look at the short-term graph we visualize the behavior from the BME measure of changing the minimum. The first big climb following the graph has occurred from 0.0035 to 0.0091 approximately, being 261% of the initial value. This would have completed the first cycle of Fibonnaci and then corrected 30% to 0.0069 representing a 30% approximate drop. After the big climb would come another rise of the same draft, going from 0.007-0.008 to 0.0146 assuming a similar percentage.

Then I would have made the same 30% drop taking 0.0104 a great support that is being respected. Right now there would be a few days of accumulation in which the stock could rise slightly until reaching the value of the first rebound 0.0119 to start the big comeback. If we look at the previous two increases this rise could represent 261% on the lowest value that has touched, that is to say 0.0097, being very close to 0.025 €. Having a resistance value of 0.024 € as a reference value, an advisable exit value is around 0.023 €.

This would lead to a capitalization of the company of about 500 million euros. A fairly modest value for the real value of the company. In fact, it is the value that many of us put when he started to walk after two years of blockade (2015-2017). That would be the km0 of the new Abengoa and where it would be necessary to begin to analyze the value with more rigor and that I do not think it will reach until the end of the year.

Right now, cleared the clouds of creditors, and the only challenging is to continue signing contracts, end the few divestments left that will leave the net short-term debt around 1,000 million and finish the projects that are currently in.

© 2016 - All Rights Reserved - Diseñada por Sergio López Martínez

![[Valid RSS]](https://www.onepointsync.com/wp-content/uploads/2016/08/valid-rss-rogers.png "Validate my RSS feed")