Duro Felguera is one of the oldest companies in Spain. It started in 1857 as a steel company and would start production in 1860. Until 100 years ago it would not start exporting to other countries.

Duro Felguera would survive the post-war crisis thanks to an autoarchic program that was what it was in Franco's time. He would invest all his efforts in creating his own machines and workshops, as well as materials coming from the mines and tools for the shipyard and the factories.

After 20 years of swelling its own resources, it would be dedicated to selling and exporting to other companies in the national market. From 1965, it would increase its international line and cease to be a purely manufacturing company of raw materials. In this case of the main materials of the Asturian mining basins.

The opening to the outside of Duro would be progressive and come to contribute more than 95% of the total contracts in 2010. On that road would suffer several crises as in 1992, when the first Gulf War.

From that period on, it would have a very strong national presence and would increasingly be present in other countries. Its main competitor at the national level would be the Basque company Babcock-Wilcox. This company allegedly would be receiving special treatment by the socialist governments of the 80s and still would not be as strong as Duro Felguera. Even giving these supports would not survive two decades later. Hard though it would hold the pull.

The diversification of Duro Felguera at the end of the 80s would be quite large but even so it would not be able to generate a large EBDITA. The Central Hispano bank, which was the largest shareholder at that time, would decide to get rid of its position in the company after the last crisis of the government of Felipe Gonzalez, an international crisis that coincided with the first Gulf War.

From the arrival of the German partner, Metallgesellchaft Duro would change dynamics, from being a manufacturer of materials or tools to being the one that would be responsible for delivering the projects "turnkey" . This would be part of the evolution of many companies in Europe, which seeing that other countries in the world manufactured more and cheaper would devote all their effort to manage projects and finalize them.

Duro had a lot of experience from below and that would give him a great strength against other competitors who had always been dedicated to managing projects and selling them, but who always depended on "how" and "what". This experience would be the result of the development of structures and machinery to carry out plants and factories in Spain for more than half a century. Thanks to this, it would soon expand to other countries having a presence where they are shown on the following map:

In 2000 the shareholders would change again, making other local investor groups and Álvarez Arrojo increase its capital in the company significantly.

In 2000 the shareholders would change again, making other local investor groups and Álvarez Arrojo increase its capital in the company significantly.

En 2015 Andres Giraldo Andres Giraldo would leave the group seeing what was to come. This manager would be responsible and much of everything that happened in the last three years. It would be from the Santander bank where the evolution of the company would have been completely controlled .

Due to the high diversification the risk of the company was already very subject to the economic situation in South America or in other countries. In Brazil in 2015 there would be an unprecedented crisis with a high devaluation of the Brazilian Real. In addition, other countries like Venezuela were starting to have problems.

And it is that that year was spent in three months one third of the total value of the company and the benefits in the first four-month period would decrease by 50% compared to the previous year. This usually happens when a company arrives at bad managers and they try to make the maximum profit in the shortest possible time , asking for loans to carry out projects or embarking to spend thinking about benefits of projects that still They are not starting. And this is what the famous Giraldo would have done in his previous years and his team, squander 100 years of a company's signature . Responsible would be the president of having appointed him, and of not having had enough caution as his father-in-law, the creator of the great Duro Felguera. And is that the succession of the same by his son-in-law would have been the last of the options he would have had but due to his state of health in recent times and want to leave the company in the hands of the family would have been finally like this.

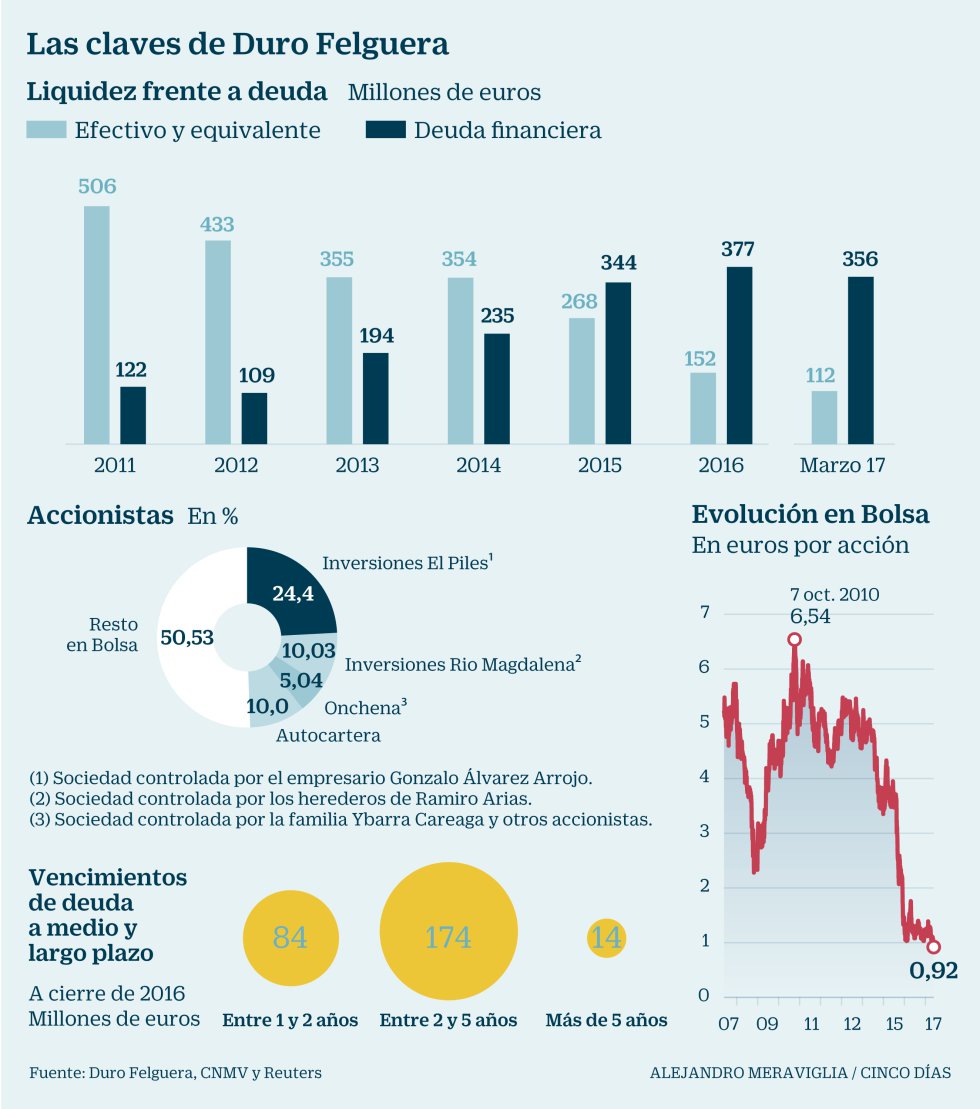

The chart on the right shows the evolution of the debt compared with the cash of the company, seeing how in 2015 they are already at the same level, starting to enter a dangerous area.

So, the worst was yet to come and due to leaving vultures in the nest, the Santander bank would become one of the main creditors of this group. Having full power to manage the company at will. It would also have all the internal information of the group to be able to make and unpack if necessary .

In 2016, despite having orders for a value greater than 2000 million debt would begin to corral Duro Felguera and banks would try to restructure that debt to be able to be paid in the future. Those involved in these adjustments would be the majority of the Spanish banking sector: Banco Santander, BBVA, CaixaBank, Popular, Banco Sabadell, Liberbank and Banco Cooperativo .

In 2017 the crisis would explode, and is that the strong debt of the company would be added problems such as a complaint for the collection of bribes to countries like Venezuela in 2009 to take contracts. These facts of the past were unmasked just when the company had more problems surely for someone who had been harmed by Duro or for interests in which the quote fell further. Already exceeding 50% of losses that year and according to the graph does not present a very forward future. And is that since 2012 the financial situation of the company would have gone downhill, being 2015 the critical year where everything would change coincident with the departure of Andres Giraldo.

Seen like this already in 2017 it would be seen that the banks wanted to save their furniture, forcing the company to bankruptcy to recover their loans to a certain extent. However, there is still the question of whether those banks would not be responsible for having left credits knowing that they were not going to be paid in order to be able to stay in the future, and that the banks have transferred withdrawals to the bank but in exchange they have received more control over the company. The purpose is to lose as little money as possible by recovering part of the loans with the works that remain to be completed, and that is where most of the money that is refinanced goes. With this the banks recover their money and also gain a position within the company which will be controlled in the future by funds and companies controlled by these banks.

This 2018 will have been one of the darkest chapters in the history of Duro Felguera. Since the highs of 2011 the capitalization of the company has gone from being worth more than 500 million to be worth about 50 million. One tenth of what it was worth, going from 6 euros to just over 50 cents.

The fat fall would occur in 2015, retreating 75% of its value. From that fall back another 50%, to reach the 0.92 euros that marked the previous graph, and hence a return to minimums. Currently it is trading at 1.2 cents per share. Seen with perspective of the old value to about 12 centimos of euro of the old shareholders. This means another dilution of almost 90%. In this way, any shareholder who had € 70,000 in this value only three years ago would not have more than € 1,000 left today. This bulky loss has not been supervised by stock regulators or by any external auditor. It is not surprising that every day more foreign funds avoid investing in Spanish listed companies and the IBEX35 is on its way to the abyss.

In any other European country this would have been cut long before it happened.

After the announcement of the expansion, Banco Santander would lead the restructuring agreement, trying to fit the largest number of shares to the retailers. In this case the play would not go well and although one day came to rise almost 200% passing the shares of 6 cents to 20 cents on the day would be neither more nor less than intraday retailers and the bank itself that had to stop that speculative move because there were not nearly people who went to that extension. The majority of investors had the memory of Abengoa, where the bank threw the stone and hid the hand, starting as the company's supporter and undoing its positions along with the rest of the banks, selling the shares that had been granted to them at the best price. , and remaining enough to have the company controlled.

In this case most of the shares are from the banks and they have not gotten anyone to give a hard for them, being the value in technical bankruptcy and being at the expense of the completion of projects to be liquidated the company. When the time comes, the creditors' meeting will be presented and their assets will be granted to the banks at the best of times.

All this capital increase and restructuring of the debt has been possible thanks to the two large historic families of the shareholders of Duro Felguera such as Inversiones Somio, with 27%, (Arrojo family) and Inversiones Rio Magdalena, 11% (Arias family), they have not attended the extension as a condition of the banks . And it is that like in Abengoa with the Benjumea, the banks take justice into their own hands and in the end if you do not pay what you owe they take you out of the way.

One more proof of how swollen the capitalization of the company was before the expansion is explained by the rise to 23 cents of the company that after the expansion could reach almost 1,500 million. This was a mere stratagem by banks to try to strip any retailer. A practice that should have been investigated by the CNMV.

Just before the widening, the stock would fall to lows again, going from 23 cents to 2 cents. And is that giving a company the value for the shares when there was 97% of new shares that were in the form of law is a practice where the word speculation falls short and where other words such as fraud or theft come in .

But the worst was yet to come because after this new injection of capital the company would present disastrous results, presenting losses of more than 50 million in a single quarter. Recall that the company was worth no more than 50 million before the disaster. Due to the new measure of the CNMV favored by the BME the minimum would be considered below the cent per share.

As soon as the measure was taken, the stock would suffer a new collapse, reaching 0.7 cents or, in other words, 0.007 €.

A capitalization of 30 million euros. After leaving the quotation in these prices in which nobody dares to justify its value since knowing that it is in technical bankruptcy and that the value is negative, I ask myself the following questions.

| ### | 2014 | 2015 | 2016 | 2017 | 2018 |

|---|---|---|---|---|---|

| Debt/Cash company | Total Debt (M) | -175 | -209 | 170 | 252 | 85 |

| Benefit/Share Value | |||||

| Capitalization(M) | 536 | 211 | 179 | 52,8 | 61[Tras Ak] |

| EBDITA (M) | 69 | 76 | 34 | -135 | 11 |

| Net Benefit (M) | - | -69 | -19 | -175 | -80 |

| Dividend (M) | - | 1.152 | 1.152 | .. | .. |

If we analyze the value in the long-term plane we observe how there are three great moments.

From there the banks would play with the value trying to make an Abengoa in Duro Felguera without having much success. And is that the price prior to the increase would rise from 0.02 € to 0.23 € representing a quotation equivalent to 1,500 million. In Abengoa the same thing happened and the CNMV did not take letters, but nobody would expect that 1 year later the same thing would happen. However, Abengoa would be worth virtually that value after dilution but we are talking about a company with dimensions 20 times greater than Duro Felguera is so it could have some meaning. In this case the only possible reasoning is that the banks currently have control of the CNMV . The regulatory body does what they want it to do.

From the following graph you can draw the following conclusion. The price of Duro Felguera should have been suspended in December 2015 and not have reopened until right now with the loss of the value of the stock to the former owners and leaving time for possible claims for negligence.

© 2016 - All Rights Reserved - Diseñada por Sergio López Martínez

![[Valid RSS]](https://www.onepointsync.com/wp-content/uploads/2016/08/valid-rss-rogers.png "Validate my RSS feed")